Kraft Heinz Earnings: Reset Year Sets Stage for Volume Recovery

- Feb 11

- 4 min read

TL;DR

Revenue Strength: Organic sales declined as volume pressure continued, particularly in North America retail.

Margin Trends: Inflation, investments, and impairment charges weighed on profitability.

Forward Outlook: Management is prioritizing brand investment and execution to drive volume-led recovery.

Business Overview

The Kraft Heinz Company is a global food and beverage manufacturer with approximately $25 billion in annual sales, operating across North America, International Developed Markets, and Emerging Markets.

Its portfolio includes iconic brands such as Heinz, Kraft, Oscar Mayer, Philadelphia, Capri Sun, and Lunchables, organized across consumer-driven product platforms including Taste Elevation, Easy Meals, and Emerging Markets growth brands.

The company maintains exposure across retail grocery, away-from-home foodservice, and international distribution channels, with North America representing the largest revenue contributor.

Kraft Heinz Earnings Performance

Revenue

Fourth-quarter net sales declined 3.4% to $6.35 billion, with organic net sales down 4.2%, driven primarily by volume/mix declines of 4.7 percentage points.

For the full year:

Reported net sales: $24.9 billion (down 3.5%)

Organic net sales: down 3.4%

Volume declines were concentrated in coffee, cold cuts, frozen meals, snacks, bacon, condiments, and spoonables, while pricing contributed modest growth.

Regionally:

North America organic sales declined ~5%

International Developed Markets declined modestly

Emerging Markets grew organically ~4.6%

Margins

Fourth-quarter gross margin declined 150 basis points to 32.6%, while adjusted gross margin fell 130 basis points.

For FY2025:

Adjusted gross margin declined 120 basis points

Inflation in commodities, manufacturing, and tariffs exceeded productivity gains

Adjusted operating income declined 11.5% for the year and 15.9% in Q4.

Profitability

Fourth-quarter results:

Diluted EPS (GAAP): $0.55 (down 68.8%)

Adjusted EPS: $0.67 (down 20.2%)

Full-year results:

GAAP EPS: $(4.93), driven by impairment charges

Adjusted EPS: $2.60 (down 15%)

Operating income was significantly impacted by $9.3 billion in non-cash impairment losses.

Key Drivers

Management identified several core pressures:

Market share losses in U.S. retail

Inflation and tariffs

Increased marketing and R&D investment

Declining category traffic and consumer trade-down

“To say the least, it was quite a challenging year for the sector and Kraft Heinz.” — Steve Cahillane, Chief Executive Officer

Forward Guidance

For fiscal 2026, Kraft Heinz expects:

Organic net sales: down 1.5% to down 3.5%

Constant-currency adjusted operating income: down 14%–18%

Adjusted EPS: $1.98–$2.10

Free cash flow conversion: ~100%

Guidance reflects incremental investment of approximately $600 million across marketing, sales, pricing, and R&D.

Risks & Opportunities

Key risks include:

Commodity inflation and tariffs

SNAP-related demand headwinds (~100 basis points)

Consumer trade-down behavior

Continued U.S. retail share pressure

Opportunities include:

Emerging-market growth

Taste Elevation portfolio momentum

Productivity and working-capital improvements

Operational Performance

Despite earnings pressure, execution improved in several areas. The company delivered:

~$690 million in gross productivity savings in 2025

Free cash flow of $3.7 billion, up ~16%

Working-capital improvements driven by inventory management

“Productivity savings continue to be a bright spot, reflecting discipline and end-to-end improvements across manufacturing, logistics, and procurement.” — Andre Maciel, Chief Global Financial Officer

Execution challenges remain most pronounced in North America retail and Indonesia distribution recovery.

Consumer Demand, Pricing, and Category Dynamics

Management described a soft consumer environment with elevated trade-down behavior, particularly in foodservice and U.S. retail categories.

Volume declines were concentrated in:

Lunchables

Spoonables

Frozen meals and snacks

Pricing remained modestly positive but insufficient to offset volume declines.

“We took pricing to address double-digit inflation… We need to earn our price by providing consumers with more value and product differentiation.” — Steve Cahillane, Chief Executive Officer

Category takeaway: Kraft Heinz is transitioning from price-led revenue management to value- and volume-led recovery, signaling a shift toward consumer reinvestment after several years of defensive pricing.

Strategic Initiatives

Management outlined a multi-year reset focused on brand reinvestment and innovation. Key initiatives include:

$600 million incremental investment in 2026

R&D investment increase of ~20%

Expanded marketing spend (~5.5% of net sales)

Innovation platforms focused on nutrition, convenience, and new occasions

Expansion of Heinz into new categories and geographies

Examples include:

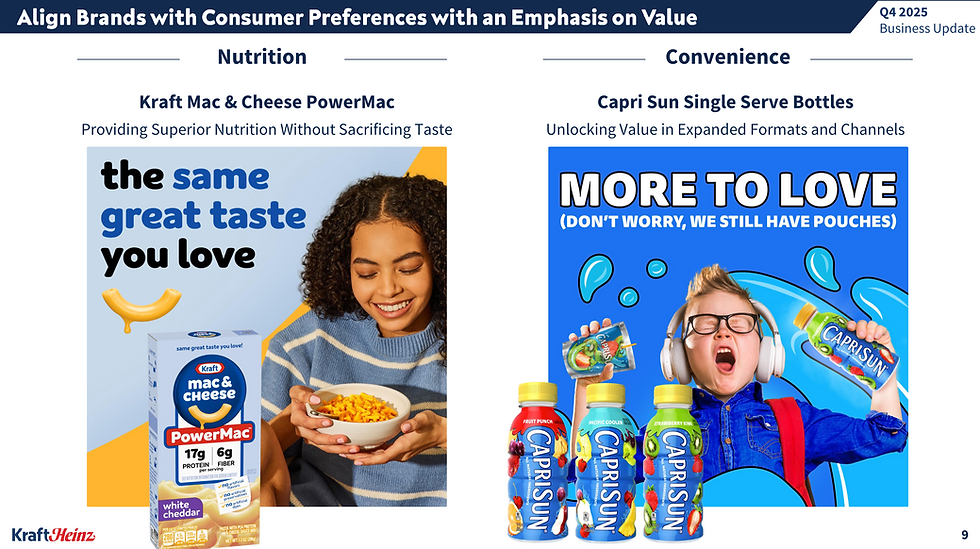

Kraft Mac & Cheese “Power Mac”

Capri Sun single-serve bottles

Heinz pasta sauce expansion

Management also paused the planned corporate separation to focus resources on business recovery.

“My number one priority is returning the business to profitable growth.” — Steve Cahillane, Chief Executive Officer

Capital Allocation

$1.9 billion in dividends paid in 2025

~$400 million in share repurchases

Remaining repurchase authorization: ~$1.5 billion

Net leverage maintained near 3×

Management plans to prioritize:

Investment in the business

Debt reduction

Portfolio management

Shareholder returns

The Bottom Line

Kraft Heinz’s 2025 results reflect a transition year marked by volume pressure, margin compression, and portfolio impairment charges.

Three key investor takeaways:

Volume recovery is now the central strategic objective, replacing pricing as the primary lever.

The $600 million reinvestment plan represents a structural reset, not a tactical adjustment.

Execution in North America retail and innovation cadence will determine the turnaround trajectory.

The company’s strong cash generation and balance sheet provide flexibility, but the investment cycle will likely pressure near-term earnings. This quarter signals a shift from cost discipline toward growth reinvestment — a necessary but risky phase in Kraft Heinz’s transformation.

—

Stay informed. We break down earnings, trends, and policy shifts shaping consumer staples and adjacent industries — no paywalls, no newsletters, just actionable insights wherever you scroll. Follow us on LinkedIn and X for more.

Comments