Wingstop Earnings: Record Openings Offset by Same-Store Sales Dip, Smart Kitchen Drives Margin Gains

- Nov 5, 2025

- 4 min read

TLDR

• Revenue Strength: Total revenue rose 8.1% to $175.7M, driven by 114 new openings and higher advertising fees.

• Margin Trends: Adjusted EBITDA surged 18.6% to a record $63.7M, with company-owned restaurant margins improving 300 bps on lower chicken costs.

• Forward Outlook: Management lowered comp guidance for 2025 but reaffirmed confidence in long-term growth, citing the rollout of Wingstop Smart Kitchen and loyalty platform Club Wingstop to drive 2026 recovery.

Business Overview

Wingstop Inc. (NASDAQ: WING) is a fast-growing global restaurant brand specializing in cooked-to-order, hand-sauced chicken wings, tenders, and sandwiches in 12 signature flavors. Headquartered in Dallas, the company operates an asset-light franchise model, with over 2,900 restaurants worldwide, 98% of which are franchised. Its domestic average unit volume (AUV) stands at $2.1 million, and digital channels account for nearly 73% of total sales.

Wingstop Earnings

Wingstop delivered another quarter of strong top-line expansion and record profitability:

System-wide sales grew 10% year-over-year to $1.4 billion, fueled by robust unit growth.

Total revenue increased 8.1% to $175.7 million, supported by higher advertising fees and franchise development, partially offset by a 5.6% decline in domestic same-store sales.

Adjusted EBITDA rose 18.6% to $63.7 million, the highest in company history.

Net income climbed 10.7% to $28.5 million ($1.02 per diluted share), while adjusted EPS reached $1.09, up 15.6%.

Margins: Cost of sales as a percentage of company-owned revenue improved to 74.8% from 77.8%, reflecting sales leverage and lower chicken wing prices. SG&A decreased by $1.6 million due to reduced incentive compensation, despite system implementation costs tied to a new ERP and HR platform.

Forward Guidance

Wingstop adjusted its 2025 outlook to reflect consumer softness:

Domestic same-store sales: Now expected to decline 3%–4% (previously +1%).

Global net new units: 475–485 openings, up from prior 17–18% growth outlook.

SG&A: $131–132M, including ~$4.5M in system implementation costs.

Interest expense: $37.5M (down slightly from $39M).

CFO Alex Kaloi noted, “Our fundamentals remain strong, and we believe 2026 will mark a return to same-store sales growth as Smart Kitchen and Club Wingstop roll out nationally.”

Operational Performance

Wingstop’s expansion engine remained on full throttle:

114 net new restaurants opened in Q3—its fifth straight quarter of 100+ openings.

Global count reached 2,932 units, including 427 international.

Company-owned stores posted 3.8% same-store growth, outperforming the system.

CEO Michael Skipworth emphasized the transformative impact of Wingstop Smart Kitchen, saying, “We are seeing more restaurants deliver 10-minute speed of service—a 50% reduction from prior levels—with 100% of them improving guest satisfaction.”

Margins also benefited from efficiency gains in these Smart Kitchen markets, with the Southwest region outperforming system averages by mid-single digits.

Market Insights

Management cited a broad-based softening in industry traffic, particularly among Hispanic and low-income consumers, though the higher-income cohort ($75K+) showed growth. Skipworth framed this as cyclical rather than structural:

“We believe this is only temporary, and the current consumer environment will prove to be cyclical.”

Wingstop’s dinner daypart continues to expand, and digital penetration above 70% positions the brand well for long-term engagement and targeted marketing.

Consumer Behavior & Sentiment

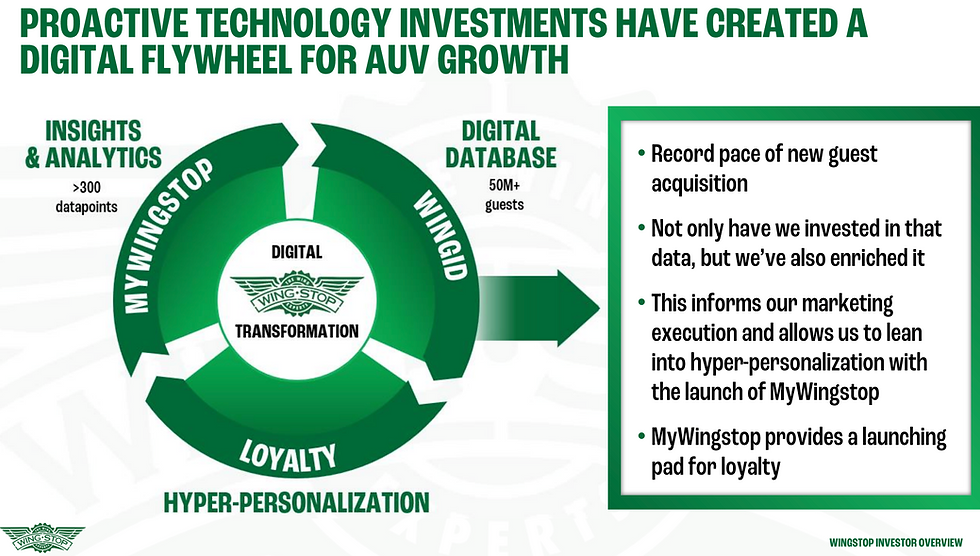

Despite near-term consumer strain, brand health metrics remain strong. Wingstop continues to win favor with higher-income consumers while piloting Club Wingstop, a loyalty program leveraging 60 million digital users to personalize offers and deepen retention.

“Club Wingstop will bring a hyper-personalized digital experience to life—not through discounting, but through curated access to flavors, content, and experiences,” said Skipworth.

Strategic Initiatives

Wingstop’s growth playbook centers on three pillars:

Smart Kitchen Rollout: Completed in over 2,000 restaurants, targeting full U.S. deployment by year-end 2025 to improve speed, consistency, and satisfaction.

New Marketing Campaign: “Wingstop is here” aims to bridge a 20% brand awareness gap, showcasing everyday occasions and leveraging partnerships like the NBA.

Loyalty Launch: Club Wingstop goes national in mid-2026, integrating with the MyWingstop platform to drive frequency.

International growth remains a key vector, with recent expansion in France, the Netherlands, GCC markets, and a new landmark franchise agreement in India, which carries 1,000-restaurant potential.

Capital Allocation

Wingstop continues to balance aggressive growth with shareholder returns:

Dividend: $0.30/share, payable Dec 12, 2025.

Share Repurchases: 140,103 shares repurchased in Q3 at an average price of $285.26.

Remaining authorization: $151.3 million under its existing buyback plan.

Since 2023, the company has repurchased over 2.3 million shares at an average price of $260.45, returning $1 billion+ to shareholders over the past decade.

The Bottom Line

Wingstop’s Q3 proves the brand’s playbook still works — record openings, record margins, and a clear runway to scale toward $3M AUVs and 10,000 restaurants. The short-term dip in comps looks cyclical, not structural, with Smart Kitchen, Club Wingstop, and the new “Wingstop is here” campaign setting the stage for a demand re-acceleration in 2026.

Key investor watchpoints:

Comps Velocity: Track how quickly same-store sales inflect as Smart Kitchen efficiency and marketing awareness feed through the system.

Digital ROI: Measure engagement, frequency, and incremental spend once Club Wingstop loyalty goes national — a litmus test for the brand’s data flywheel.

Margin Resilience: Monitor wing costs, SG&A discipline, and pricing restraint to see if record EBITDA margins hold through a softer consumer cycle.

Unit Quality over Quantity: Watch franchisee returns and international ramp quality as growth stays in the mid-teens — a key signal of durability.

Capital Returns: Gauge balance between aggressive buybacks, steady dividends, and reinvestment — Wingstop’s ability to compound without over-levering.

--

Comments